- 4D Real Estate's Weekly Roundup

- Posts

- Understanding Interest Rate Impacts

Understanding Interest Rate Impacts

Essential Insights for First-Time Buyers 📊

Donna Wade

April 30, 2024

What’s The Tea with 4D? 🍵

Hello friends!

This week, my thoughts are with all the first-time buyers out there. You may have noticed that interest rates have increased slightly in recent weeks, and this can significantly affect new buyers. You might be wondering: How exactly do these interest rate changes influence what a buyer can afford?

Here’s an example to answer that question! Mortgage interest is a percentage of the balance of what you owe on a home. There is the initial loan amount. For this example, let’s say the home is $400,000 and the loan being utilized is a 30-year, fixed-interest rate loan. When you start making your house payment, most of your payment will be applied to the interest on the loan. As you continue to make payments over the years, the amount of your payment that starts to be applied to the principal increases.

So, as a buyer, the amount you will end up paying for your home changes based on the interest rate that you have to pay on the loan itself. You will pay more for a home priced at $400,000 at a 7% interest rate than you will for a home priced at $400,000 with an interest rate of 5%, for example.

So, with rising rates, is it still a good time for new buyers to get into the market? The answer is likely yes for a variety of reasons. First, there are specific loan programs geared towards assisting first-time buyers with their costs. There are loans with down payment assistance or closing cost assistance. Also, interest rates continue to vary, and have the potential to decrease over time. When they do, that may be a great time to refinance the home loan and get a better rate, thus lowering the monthly payment and longer-term cost of your loan.

One of the primary benefits of purchasing a home now is the opportunity to begin building equity. As your property appreciates in value and you steadily pay down the loan, you accumulate equity in your home. This equity serves as a valuable asset, providing options for future investments, funding home improvements, or even facilitating the purchase of another property should you decide to sell.

When it's time to make a move, you'll have that equity to use towards the purchase of your next home. Taking the example of a $400,000 home owned for 5 years, let's assume its market value rises to $460,000 during that period, while the loan balance decreases to $379,000 through regular payments. Upon selling the house, you can calculate your profit by subtracting the current market value from what you still owe, and then deducting seller fees. This chunk of profit will serve as a valuable down payment for your next home.

First-time buyers are some of my favorite folks to help! It’s a wonderful time when you make the leap from building someone else’s security by paying rent to building your own by paying a mortgage.

How To Keep Track of Mortgage Rate Trends

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

The Latest on Mortgage Rates

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

Professionals Can Help Make Sense of it All

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of time and effort. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, connect with a reputable local realtor (like 4D Real Estate) and let them do the work for you!

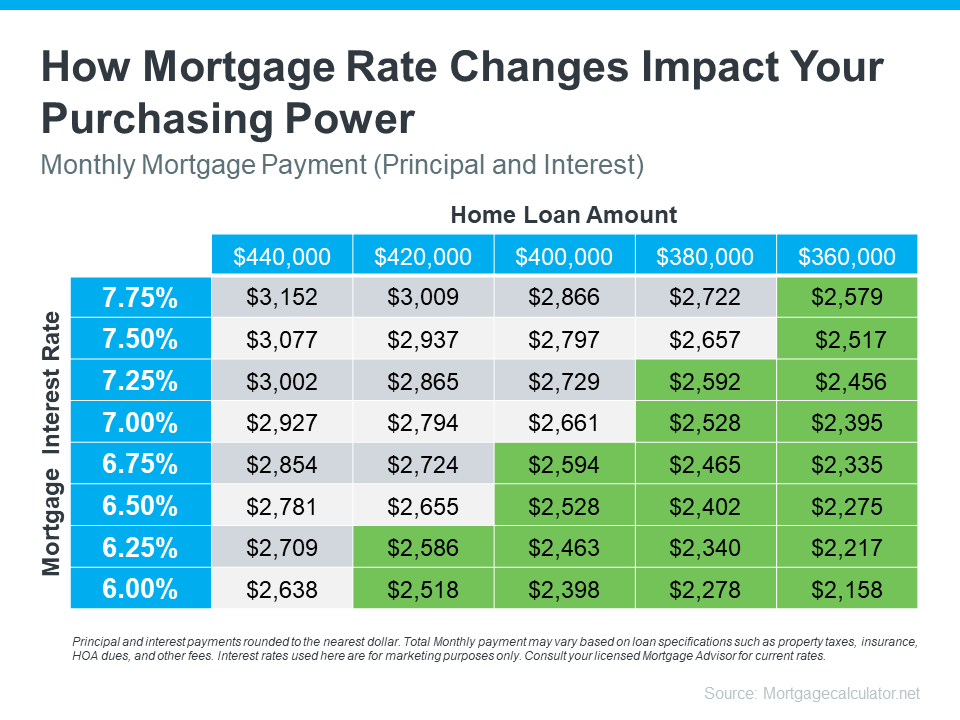

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford.

Let's chat over coffee to discuss more details and address any questions you may have about the current market. And your first cup is on me! ☕️

Click below to book a date and time that works best for your schedule. After booking, I'll reach out to confirm the location. I look forward to connecting with you soon! 😊